Authors

Micah Rabin

Research Intern

Overview

In January 2022, Microsoft announced that it will acquire gaming giant Activision Blizzard for $68 billion—the largest acquisition ever in the tech sector. However, the deal could run into trouble as US legislators and regulators look to restrict large technology firms from buying other companies due to concerns over reduced competition.

Background

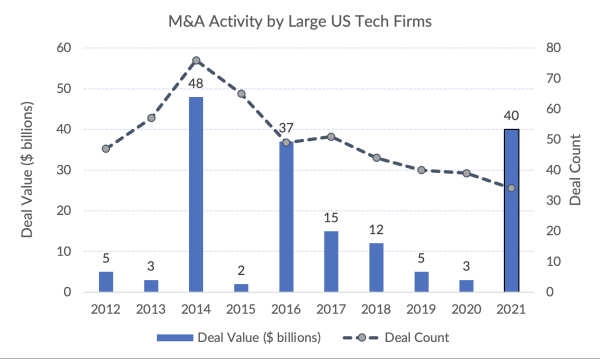

In 2021, merger and acquisition (M&A) activity by the largest US tech firms reached a seven-year high, with Amazon, Alphabet, Apple, Meta, and Microsoft collectively spending $40 billion (see graph below). High-profile acquisitions included Amazon’s $8.5 billion purchase of MGM Studios.

As large tech firms continue to expand, so too has a belief in Congress and the White House that more needs to be done to bring greater competition to the digital economy. Of the few competition tools the government has available, reviewing M&A transactions is arguably the most impactful. The Federal Trade Commission (FTC) and the Antitrust Division of the Department of Justice (DOJ) are the two agencies responsible for reviewing mergers and, if appropriate, can attempt to block or unwind them in federal court.

While Microsoft’s deal comes at a politically inopportune time for them, it is helped by being a vertical transaction. Unlike horizontal deals that involve a company buying a direct competitor (think Facebook buying Instagram), vertical deals involve a business purchasing a firm that it has a buyer-seller relationship with. Horizontal deals have historically been the focus of pre-merger reviews as the loss of competition is direct and measurable. However, vertical transactions have come under closer scrutiny in recent years. For example, in 2017, the DOJ filed suit to prevent a vertical deal between AT&T and Time Warner. In September 2021, the FTC voted to rescind the previous set of guidelines it used to analyze vertical deals—indicating a willingness to impose stricter rules.

Note: Companies included: Alphabet, Amazon, Apple, Meta (Facebook), Microsoft. M&A control transactions only. Lead or sole investor only. Deal dates are from 01/01/2012 to 01/01/2022. Source: Milken Institute analysis of Pitchbook data (2022).

Why Is This Important?

Microsoft’s deal with Activision comes at a time when reduced competition in the economy—particularly the digital economy—is high on the political agenda. In an Executive Order last summer, President Biden made it clear that tackling consolidated sectors was a priority for his domestic economic policy. More recently, he has blamed reduced competition for contributing to high levels of inflation, according to The New York Times. In Congress, public hearings with CEOs from the largest US tech firms have taken place, and a spate of antitrust bills have been introduced to regulate business practices—including M&A—that can contribute to consolidated market power. Finally, key vacancies at the FTC and the DOJ have been filled by Lina Khan and Jonathan Kanter, both vocal advocates of increased antitrust enforcement in the US.

What Happens Next?

As reported in The Wall Street Journal, the FTC announced that it will be responsible for reviewing Microsoft’s purchase of Activision. This deal joins several thousand others that have met the threshold for pre-merger review in the last year, a trend that has put a strain on the FTC’s limited resources. In response, the Senate passed a bill last year that would increase the FTC’s budget by raising the fee paid by companies under pre-merger review. The House recently introduced its own version of the bill, and it is expected to pass soon. In the meantime, the FTC and the DOJ announced this month that they are launching a public inquiry with the aim of tightening merger rules and enacting closer reviews of large mergers. This may well be a deterrence strategy to slow down future M&A activity.

A separate piece of legislation that could have a significant impact on the US M&A landscape is the bipartisan Platform Competition and Opportunity Act (S. 3197, H.R. 3826). If passed, this would reverse the burden of proof by instead requiring the dominant company in an acquisition to prove that the deal would not substantially harm competition.

For questions, please contact [email protected].

Authors